Stuck in the ’80s: why Europe’s retail giants can’t keep up with Walmart’s digital revolution

A decade ago, Walmart's extensive network of physical stores seemed like a liability in an era dominated by online shopping. As Amazon quickly rose to prominence with its user-friendly e-commerce platform and vast inventory, many industry analysts predicted Walmart's decline. However, Walmart not only withstood the challenge but also strategically transformed itself into a digital powerhouse, turning its physical stores into valuable assets rather than burdens. Today, Walmart is the world's largest company in terms of revenue, maintaining its dominance while also emerging as a strong competitor to Amazon in the e-commerce sector. This transformation reflects a larger disruption within the retail industry, where changing consumer behaviour, the rise of e-commerce, and the influence of discount stores are reshaping traditional retail models.

One of the key factors behind Walmart's resurgence is its successful implementation of an omnichannel approach. Unlike Amazon, which primarily operates online, Walmart has integrated its extensive network of 4,700 U.S. stores into its digital ecosystem. This strategy enables customers to purchase products online and choose either to pick them up in-store or have them delivered directly from local outlets. By repurposing its physical locations as distribution hubs, Walmart has significantly reduced shipping times and costs. Approximately 90% of Americans live within 10 miles of a Walmart store, giving the company a logistical advantage over Amazon, which relies on centralized fulfilment centres. This hybrid model not only lowers logistics costs but also addresses the challenge of last-mile delivery, a significant pain point for e-commerce companies that operate solely online.

Walmart's strategic focus on cost efficiency is a crucial element of its competitive advantage. This approach enables the company to uphold its reputation for everyday low prices while simultaneously investing in digital transformation. John David Rainey, Walmart's Chief Financial Officer, highlighted the significance of cost leadership, stating, "We want customers to think of us as the place to go to get the lowest prices on anything they want to buy. To do that, we have to have the lowest cost to serve."

Walmart has experienced remarkable growth in e-commerce. In the third quarter of 2024, U.S. e-commerce sales surged by 22%, largely due to the popularity of store-fulfilled pickup and delivery services. Presently, 18% of Walmart's revenue is derived from online sales, and its marketplace features over 700 million items from third-party merchants. This rapid digital transformation has solidified Walmart's position as a significant player in the e-commerce sector.

To compete directly with Amazon Prime, Walmart introduced Walmart+, a subscription service that offers free same-day delivery, fuel discounts, and exclusive promotions. Walmart+ has successfully attracted higher-income customers, with households earning over $100,000 accounting for 75% of Walmart's recent market share gains. By providing valuable perks at a competitive price, Walmart+ has enhanced customer loyalty and increased purchase frequency.

According to John Furner, CEO of Walmart U.S., “We want to be the low-cost provider, but we also want to offer the best convenience.” This dual focus on cost leadership and customer convenience has been a driving force behind Walmart’s strategic decisions, positioning the company as a formidable competitor to Amazon's Prime membership model.

A significant part of Walmart’s strategic resurgence involves substantial investments in technology and automation. The company has integrated advanced data analytics, artificial intelligence (AI), and robotics into its operations to improve efficiency and enhance the customer experience. In its U.S. regional distribution centers, robots categorize and assemble pallets by department, which accelerates the stocking process in stores. Additionally, AI tools optimize workforce management, reducing shift planning time from an hour to just five minutes. By leveraging these technologies, Walmart not only boosts operational efficiency but also lowers costs, further contributing to its competitive pricing advantage.

This transformation goes beyond just operational efficiency; it is also about redefining Walmart's identity within the retail industry. As Nikki Baird, Vice President of Strategy and Product at Aptos, observed, “Walmart is rapidly transforming itself into a tech company akin to Amazon. I view these two companies as being in a category by themselves, while everyone else remains in the retail sector.”

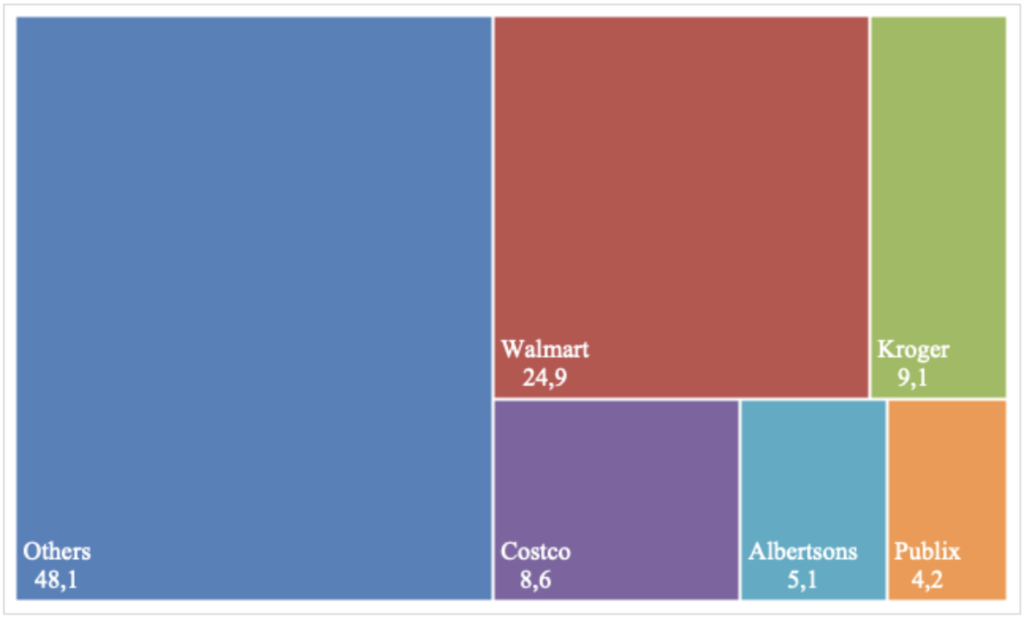

One of the most notable differences between the retail markets in the U.S. and Europe is the level of market concentration. In the U.S., Walmart accounts for nearly a quarter of all grocery sales, holding a market share of 24.9%. Following Walmart are Kroger at 9.1%, Costco at 8.6%, Albertsons at 5.1%, and Publix at 4.2%, while the remaining 48.1% is shared among other retailers (seen in Figure 1). This varied landscape contrasts significantly with European markets, where a few major players dominate. In Switzerland, for instance, Migros and Coop control over 70% of the grocery market, creating a virtual duopoly that restricts competition and innovation. The UK is similarly concentrated, with Tesco and Sainsbury's combined market share exceeding 40%. In Italy, Esselunga leads alongside Coop and Conad, leaving limited opportunities for other competitors to challenge their positions. Germany is dominated by discount retailers Aldi and Lidl, who maintain significant control with their low-cost, high-efficiency business models.

This high level of market concentration in Europe creates barriers to entry and diminishes competitive pressure, leading to slower innovation and digital adoption. In contrast, the fragmented U.S. market promotes competition, encouraging retailers like Walmart to consistently innovate to retain their market leadership. Moreover, this lack of concentration allows Walmart to grow without facing the regulatory scrutiny that is often present in more consolidated European markets.

Figure 1: Top five grocery retailers by $ share, Oct 2023-September 2024 (%)

Source: Financial Times; Walmart includes Walmart US and Sam's Club stores

The retail landscape is undergoing a significant transformation driven by digital disruption. Consumers are increasingly favoring the convenience of online shopping, personalized experiences powered by AI, and seamless integration between digital and physical channels. Walmart has successfully leveraged these trends with its hybrid fulfilment model and robust digital ecosystem. In contrast, many European retailers have been slower to adapt due to inflexible business models and a heavy reliance on physical stores.

In highly concentrated markets such as Switzerland and Italy, leading retailers have little incentive to innovate, which has resulted in stagnation in digital adoption. Meanwhile, Tesco and Sainsbury’s have struggled with slow digital growth as they contend with high operational costs and complex supply chains. This strategic inertia has left them vulnerable to discount retailers like Aldi and Lidl, which continue to expand aggressively through cost-cutting measures and efficient store operations.

Walmart's evolution from a traditional retailer to a digital powerhouse showcases its adaptability, resilience, and vision. By utilizing its extensive physical network, investing in advanced technology, and diversifying its revenue streams, Walmart has maintained its market leadership and set new standards within the retail industry. This strategic shift has enabled Walmart to compete effectively with Amazon while solidifying its position as the world’s largest retailer by revenue. In contrast, European retailers are struggling to keep pace, hindered by market concentration and outdated business practices. John David Rainey, reflecting Walmart's commitment to continuous improvement, acknowledged, "We don’t do everything perfectly here. And there are many lessons we can learn from our competitors."

As digital disruption continues to reshape the industry, European retailers face a clear choice: adapt or risk becoming irrelevant. Walmart's journey serves as an inspiring blueprint for the future of retail, demonstrating that strategic foresight and digital innovation are essential for survival in an ever-changing market. While Europe remains anchored in the past, Walmart is already paving the way for the future.

Fonte